The Section 24 tax changes, introduced in 2015 and gradually implemented over four years, have reshaped the landscape for private landlords in the UK. These changes limit tax relief on finance costs for residential property investors to the basic rate of Income Tax. As we delve into the impact and implications of Section 24, it becomes clear that property investors must adapt to a new tax environment.

Understanding Section 24

Section 24, enacted as part of the Finances Act 2015 and effective from the tax year 2020, has significant implications for landlords. In the pre-Section 24 era, landlords could deduct mortgage interest and other property financing costs from their rental profits before calculating their tax liability. However, these expenses can no longer be deducted pre-tax, resulting in landlords paying tax on the full rental income and then claiming back only a portion through a tax credit.

Impact on Buy-to-Let Landlords

Buy-to-Let landlords have long relied on mortgage financing to expand their property portfolios and make improvements. This leveraging strategy allowed for efficient capital use. However, Section 24 has introduced complications, altering the financial dynamics for these landlords.

Additionally, landlords who previously relied on capital appreciation and remortgaging to support their lifestyle expenses are now facing challenges. The combined impact of Section 24 and stricter regulations imposed by the Prudential Regulation Authority has made funding lifestyle expenses through property investment less viable.

As a result of these changes, the private rental sector is undergoing a transformation. Some landlords are exiting the market, while others are seizing opportunities to expand their property portfolios.

Assessing the Impact on Your Property Business

For basic rate taxpayers, the immediate financial impact of Section 24 is limited. They will pay income tax at the rate of 20% and receive a 20% tax credit on their finance costs, effectively balancing out the tax implications.

However, higher rate taxpayers face a significant tax increase, with at least 20p of additional tax for every pound of interest paid. This shift in tax liability necessitates careful financial planning and consideration of property deals.

Regardless of your tax status, proactive forecasting is crucial. Some landlords may find themselves pushed into higher tax brackets, experiencing a substantial rise in taxable profit, which in some cases has surged by as much as 400%.

Cashflow Considerations

Many landlords may encounter cashflow challenges due to their delayed response to Section 24. The intricacies of the UK tax system mean that 2022, in particular, presents a significant cashflow hurdle. The delay in tax payments catching up with actual tax bills exacerbates this challenge.

To address these potential cashflow issues, landlords must engage in proactive financial planning. Being prepared for the evolving tax landscape and its impact on rental income is essential to navigate the hurdles ahead.

Finance Costs Defined Under Section 24

Section 24 primarily affects the financial expenses of residential landlords. These expenses include:

- Mortgage interest

- Interest on loans used for furnishing

- Fees related to mortgage or loan origination and repayment

It’s crucial to note that tax relief typically does not extend to capital repayments of mortgages or loans. The tax credit specifically applies to the finance costs disallowed under Section 24, highlighting the importance of understanding the precise scope of these tax changes.

Impact on Different Business Structures

Limited companies holding residential property can still claim finance costs as an allowable expense. However, sole traders and partnerships, including Limited Liability Partnerships (LLPs), are impacted by Section 24. In some cases, a Limited Liability Partnership may be connected with a Limited Company, effectively allowing for deductible interest. This strategic approach, often referred to as a Hybrid Business Structure or Mixed Partnership LLP, can optimize the benefits of running a professional property business.

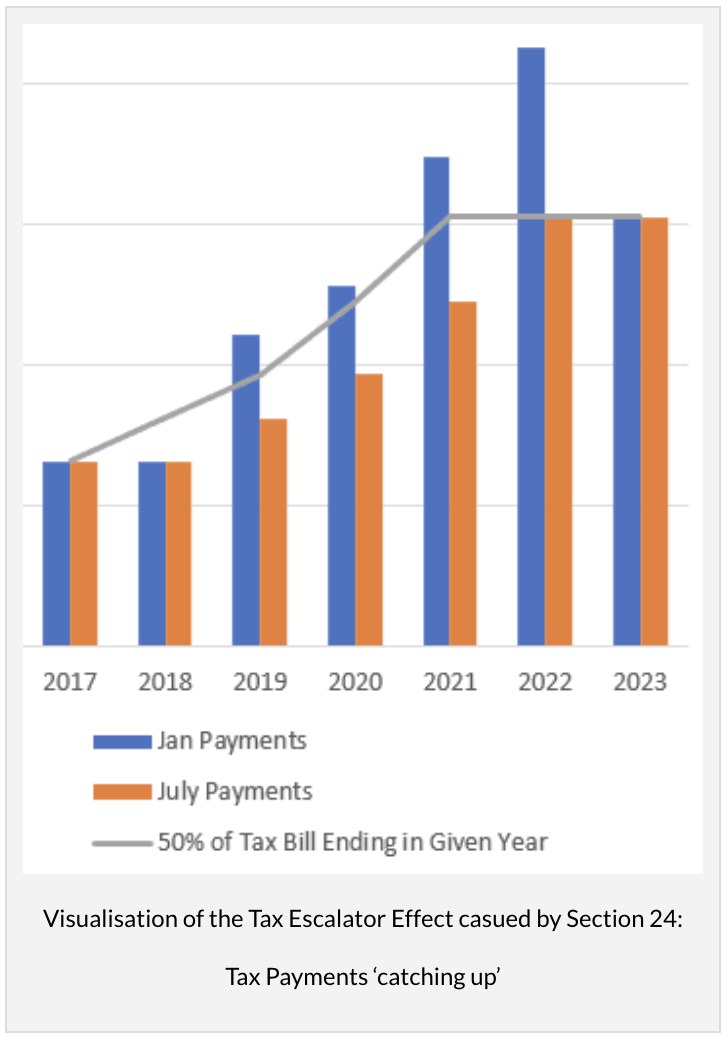

How will Section 24 impact cashflow?

Many landlords may face a cashflow crisis in the coming years due to their delayed response to Section 24, a concern rooted in the workings of the UK tax system. The graph illustrates that 2022 presents the most challenging year in terms of cashflow. The lag in tax payments catching up with actual tax bills contributes to this predicament.

This cashflow challenge highlights the importance of proactive financial planning for landlords. Being prepared for the evolving tax landscape and its impact on rental income is crucial to navigate the potential hurdles that lie ahead.

How to Reduce the Impact of Section 24

Mitigating the impact of Section 24 requires careful consideration and strategic actions. Here are some options for landlords to explore:

1. Reduce Operating Costs: Property management expenses can be trimmed by transitioning from a property management company to self-management, resulting in significant cost savings.

2. Refinance Properties: Given the current low-interest rates following the post-pandemic economic recovery, refinancing properties to secure better financing rates is a viable strategy.

3. Explore Commercial Properties or Holiday Lets: Section 24 exclusively applies to residential properties. Shifting investments to commercial properties or holiday lets can help bypass these tax changes, but careful evaluation is essential.

4. Incorporate Properties into a Limited Company: Limited companies are not subject to Section 24. Incorporating your properties into a company can help avoid this tax change, although it involves various costs such as stamp duty and capital gains tax when transferring properties.

5. Beneficial Interest Company Trust: This structure enables you to transfer your portfolio while bypassing Section 24 tax changes and maintaining personal ownership. However, it introduces considerations like corporation tax and potential remortgaging challenges, making professional advice crucial.

6. Consider Rent Increases: Incremental rent adjustments may help offset Section 24-related expenses, but careful analysis is necessary to avoid entering a higher tax bracket.

7. Portfolio Optimization: Evaluate each property’s financial performance and consider selling underperforming assets to streamline your investments in the current economic climate.

Navigating Section 24 is essential for property investors to adapt to the evolving tax landscape effectively. Each landlord’s situation is unique, and a tailored strategy is key to ensuring financial stability and growth in this changed environment.

MORE Property blogs HERE:

Buy To Let Defaults Surge with Rising Rates

Cashing Out of Buy To Let? Top Places to Make a Quick Sale

Why Are Buy-to-Let Mortgages Interest Only?

Is Buy-to-Let Still Profitable Today?

A Comprehensive Guide to Buy-to-Let Mortgages

First-Time Buyer’s Guide to Buy-to-Let Mortgages

Should You Invest in Property Now or Wait for 2024?

How Much Do You Need for Buy-to-Let Mortgages?

Stamp Duty on Buy-to-Let Properties

Can I Use Equity As A Deposit For Buy To Let?

Can I Buy A House And Renting It Out UK?

Is renting houses profitable UK in 2023?